(855) 304-3748

(855) 304-3748 Email Us

Email Us Schedule a Call

Schedule a Call

Why This Works Better Than The 4% Rule For Retirees

Determining how much money you’ll need to save now and then withdraw each year in retirement can be one of the most overwhelming elements of retirement planning. There are countless theories and strategies to most appropriately estimate how much money you’ll need in retirement and how much you can spend each year.

One of the more common principles is the 4% Rule. This retirement planning principle works as follows: a retiree household withdraws 4% of their retirement savings in year one of retirement and continues to withdraw at a rate of 4% annually. As their account balances grow, while the withdrawal rate remains fixed at 4%, the annual withdrawal amount increases to keep pace with inflation.

However, in order for the 4% Rule to “work,” two conditions must be met. First, the retiree must invest in a way that will allow his or her retirement savings to grow along with inflation. Second, there must not be a sideways or bear market occurring. (1)

Because of these conditions and other elements, the 4% Rule is by no means rock solid, and there are critics of this withdrawal principle. Not all retiree households can strictly follow a 4% withdrawal rate, especially since dividends and required minimum contributions could increase the annual withdrawal percentages. Also, the 4% Rule was created in the 1990s when interest rates were much higher than they are today.

An Alternative to the 4% Rule

For CRNAs approaching retirement, an alternative method to the 4% Rule is to base your retirement needs on the fair value today. The asset manager BlackRock tracked how much it will cost for investors to create an income in retirement via a series of indices they developed, which they call CoRI (Cost of Retirement Income). The CoRI indices consider how retirement income can change based on interest rates and inflation. (2)

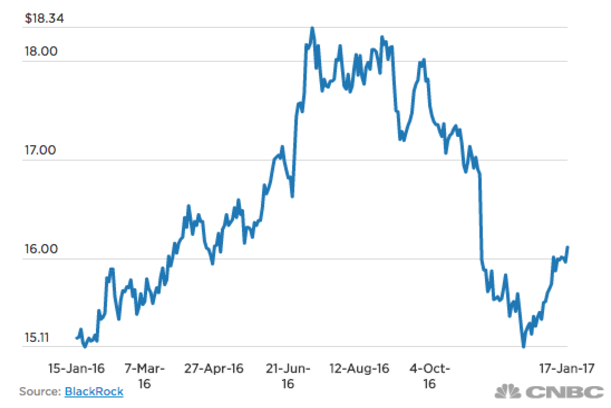

The BlackRock theory states that not knowing the fair value today of your future retirement needs would be akin to purchasing a home without knowing what the mortgage would be. As you can see in BlackRock’s chart below, the 2025 index estimates the costs now to purchase $1 of income if you plan to retire in 2025.

Based on this index, it’s estimated that investors retiring in 2025 would need roughly $16 today for $1 of income when they retire in eight years. Let’s say you want a retirement income of $100,000 each year when you retire in 2025. According to this index, you would need to multiply $100,000 by $16. So, you would need $1.6 million total for a lifetime annual income of $100,000.

These are, of course, just estimates and there are no guarantees that these figures won’t change. It’s important to remember that the cost of retirement income falls when interest rates rise, and the Fed expects to increase interest rates three times over the course of 2017. If this happens, the cost of retirement income could decrease.

Which Estimate Should You Follow?

There’s no guaranteed method for estimating the exact amount of money you’ll need to last throughout retirement. Some people prefer the 4% Rule because it’s simpler to estimate a total dollar figure that you’ll need to save. But look at how different the 4% Rule figure is compared to the CoRI index! According to the CoRI index, you would need to save $1.6 million for a $100,000 annual retirement income whereas with the 4% Rule, you would need $2.5 million.

Beyond these two principles, there are countless others, including the bucket method, which can help you estimate your total retirement savings needs. What’s more important to remember is that any of these estimates are just that: estimates. Determining a total retirement savings goal is helpful, but it’s a ballpark figure. From there, it’s important to determine how you use your savings and invest it, so it can last throughout your retirement.

Next Steps

If any of this sounds confusing, you’re not alone. Trying to predict your future needs is impossible, but there are strategies that can help you prepare for various scenarios. If you’re hoping to retire within the next ten years and wonder how much you’ll need to save, contact our office for a review of your current retirement strategies. We can evaluate what you’re currently doing and where you want to be in retirement, then determine appropriate strategies for pursuing your goals.

(1) www.money.cnn.com/2016/04/20/retirement/retirement-4-rule/

(2) http://www.cnbc.com/2017/01/19/why-this-index-works-better-than-the-4-percent-rule-for-retirees.html